August 2020 was a turning point in my journey as a solopreneur. It was the beginning of my transition from being a freelancer to a solopreneur. Building from grounds up literally. To banish feast famine cycles from my life forever.

Because I had been completely wiped out financially post COVID-19. I was chasing refunds on insurance premiums I had paid extra by mistake, struggling to keep up with subscriptions and essential community memberships, barely maintaining the basics. Client work had dried up. I realised that when income disappears, those fixed, unignorable costs can sink you.

Months later, I landed an amazing client — just one — that for the first time covered all my running expenses (personal living + essential overhead). Over the following six months, I began to build an emergency fund. But even in the midst of that recovery, a thought remained loud in my mind: I cannot survive another one like this.

Fast-forward to June 2024: I lost my top two clients almost simultaneously. At the same time, my husband and I were investing in a food and hospitality business — something that required additional capital, attention, and risk. Without the buffers and frameworks I’d built, losing those clients could have shattered everything.

But because I had emergency reserves, diversified income sources, and lean core expenses, I was able to maintain around 80% of the lifestyle my family is used to through that lean period.

That experience reinforced that fiscal discipline, fiscal systems, mindset, and well-being practices are not optional or luxuries for solopreneurs. they are essential survival tools.

In this article, I’ll share what I have learned, what works, and provide frameworks you can apply to build your own resilience.

Understanding Burnout & Financial Stress for Solopreneurs

Burnout for solopreneurs isn’t just “I’m tired from too many hours.” It is compounded by:

- Financial unpredictability: irregular income, client loss, variable contracts, all making planning hard.

- Lack of buffers: no savings or emergency fund, small margin between income and expenses.

- Overextension: taking on multiple roles (sales, operations, accounting, customer support), often without rest or delegation.

- Mental load and emotional stress: anxiety about paying fixed costs, worrying what happens if contracts stop, fearing lifestyle changes, etc.

These stressors feed into each other. Financial stress worsens decision fatigue, drains energy and even limits our ability to rest. To the extent that it makes us avoid long-term planning, which in turn exacerbates financial risk and burnout.

Research emphasises the importance of anchoring spending to a conservative baseline, stabilising financial decisions even in low-income months. Also, building a safety net and diversifying revenue streams are strongly correlated with lower financial anxiety.

Key Lessons From My 2020 Famine Cycle (that Helped me sustain 2024)

Here are my takeaways from my experience post COVID-19:

- Always know your “running expenses” (personal + business). When I lost those two top clients in June 2024, I was able to manage my affairs only because I already knew the expenses I could not avoid. That clarity helped me ruthlessly cut down on the avoidable expenses.

- Build an emergency reserve. After recovering from 2020, I committed to putting away surplus from good months so I could cover at least 6 months of running expenses. Aiming for 9 months. When lean times hit, I didn’t have to scramble for survival because I had breathing room.

- Diversify income. Relying on just one or two large clients is dangerously risky. I try to kep more recurring/retainer income, smaller projects, and passive/digital income where possible. Though I am not yet at a level I would like, I plan to get there slowly.

- Maintain expense discipline even during good times. It’s tempting to accumulate expensive habits when going gets good but increases in fixed overhead make falls steeper. I try to keep fixed costs minimal and variable costs under regular review.

- Automate & systematise. Things like invoicing, subscription renewals, community dues, tool payments — if they are regular, automate them or at least schedule reminders. Build systems so you have more time to work on your business.

- Nurture a positive outlook. Look at the slow periods as time for rest, strategy, up-skilling and recalibration. I have had to confront and overcome beliefs such as these: “if I’m not busy, I’m failing”; “slow months are shameful”; “if I say no to the kids due to lack of money I am failing them” and so on. And I am sure it has been no different for you. But during lean times I set boundaries, take scheduled rest, and invest time in doing things I am unable to otherwise.

My Systems in Action: the June 2024 Shock

When I lost my top two clients in June 2024, I could’ve been hit hard. But because I had been implementing the above lessons,

- I had emergency reserves which covered a significant portion of the fixed costs (running expenses) for several months, allowing time to pivot rather than panic.

- My variety of income sources meant that I didn’t drop to zero revenue immediately; the smaller, recurring incomes, and passive or smaller projects helped cushion the fall.

- My expense baseline was lean: I knew what could be reduced, what obligations were essential, which overheads were negotiable or deferrable. This allowed me to temporarily tighten without collapsing.

- My mindset was less reactive because I’d already practiced planning for worst-case. So I could make decisions calmly (e.g. scaling back non-critical spending, delaying some investments, without compromising family’s basic lifestyle).

Through this, I was able to sustain about 80% of our accustomed lifestyle while protecting emotional well-being. It didn’t feel like “just surviving”; it felt like I still had control.

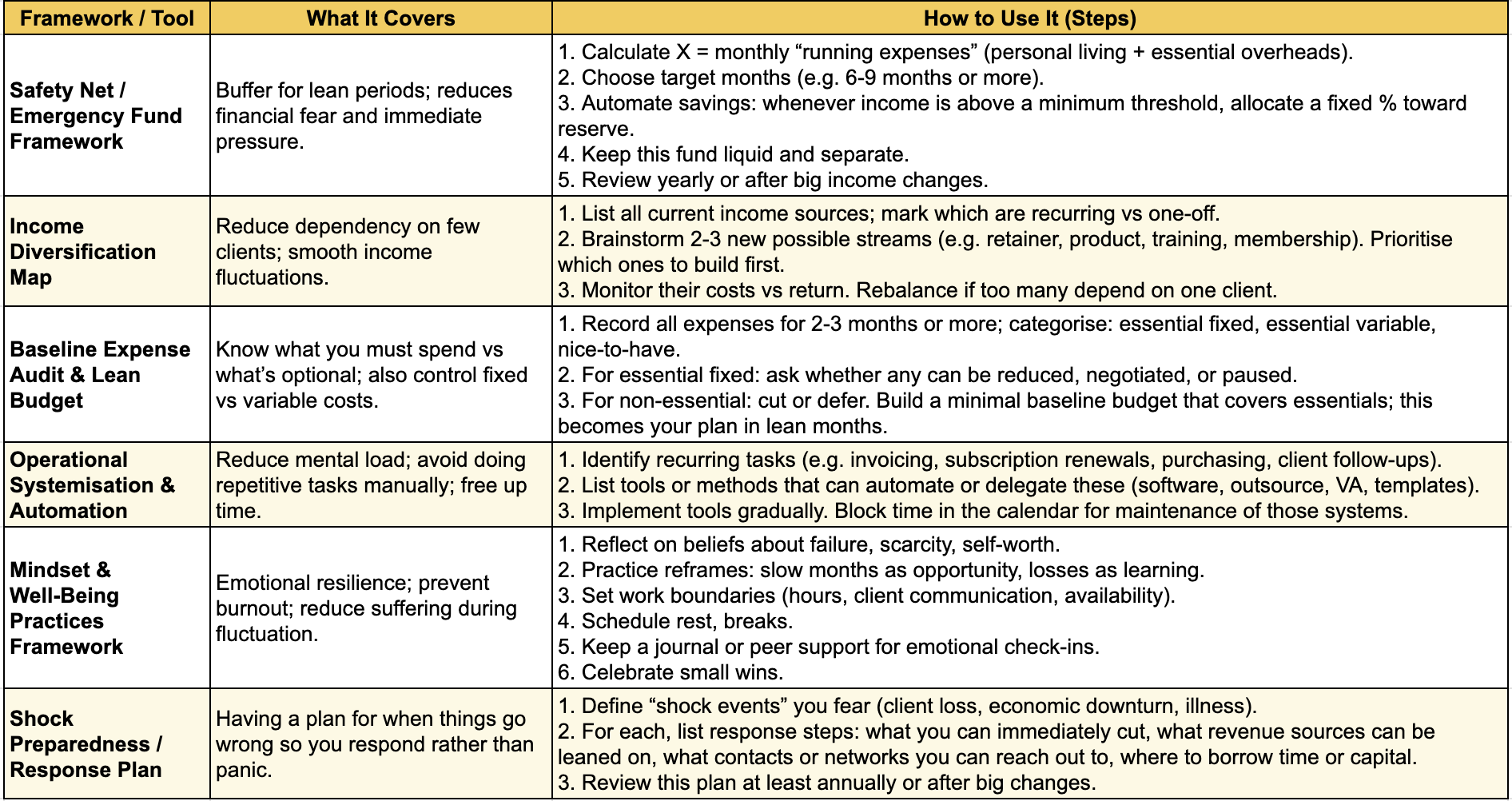

Frameworks & Tools to Build Your Financial-Wellness Systems

Here are frameworks that you can apply. They combine financial, operational, mindset, and well-being practices. You can pick ones that suit your situation.

Putting It All Together: Action Plan for Readers

Here are actionable steps you can take this month or over the next quarter to build more resilience:

- Calculate your running expenses (personal + essential overhead) → call that X.

- Set a safety net goal, e.g. 3-6 × X. Commit to starting or adding to your reserve.

- Audit your income sources → identify which are recurring, which are volatile. Plan to add at least one more stable or recurring stream.

- Do an expense audit → find non-essentials to cut or pause. Reduce fixed costs where you can.

- Automate / systematise repetitive tasks: invoicing, payments, subscription renewals, etc. Free up mental space.

- Create a shock-response plan in writing: what you’ll do if you lose a big client or have a zero month, etc.

- Mindset & well-being check: schedule rest; define working hours; find or create a community or peer group; journal on fears and growth.

Final Thoughts

Financial fragility doesn’t have to be an inevitable consequence of solopreneur life. When you pair fiscal discipline (buffers, diversified income, lean spending) with well-being practices (rest, mindset, boundaries), you build more than just a business; you build resilience.

Looking back on 2020 and again in June 2024, I see that what saved me was less about luck and more about the systems I’d put in place. Without them, losing top clients and investing in new ventures would have meant collapse. But with them, I was able to absorb those shocks, protect what matters, and preserve agency.

If there’s one takeaway: design your business for lean times as intentionally as for boom times. Because they both come—and the choice is whether you want to survive or thrive through them.

{kind=link}

Trackbacks/Pingbacks